Description and research notes

This specimen strip represents an official State of Delaware excise tax stamp issued in 1933 for beer, explicitly designated TAX PAID ON HALF BARREL OF BEER and denominated Fifty Cents. It originates from the earliest phase of state-level alcohol regulation following the repeal of national Prohibition, when individual states were forced to reconstruct taxation, licensing, and enforcement systems that had been dormant or dismantled for more than a decade.

The repeal of the Eighteenth Amendment in 1933 did not simply legalize alcohol; it transferred regulatory responsibility almost immediately to the states, many of which lacked fully developed administrative frameworks for alcohol control. Delaware responded by implementing a stamp-based excise system, in which physical tax stamps served as the primary documentary evidence that statutory taxes on alcoholic beverages had been paid. These stamps were not symbolic or decorative but functioned as enforcement tools within a fragile and rapidly evolving regulatory environment.

The specific designation HALF BARREL OF BEER situates this stamp within the wholesale and production side of the brewing industry rather than retail consumption. The half-barrel unit reflected standardized commercial brewing measures and targeted breweries and distributors operating at industrial scale. As such, this stamp represents a point where state fiscal authority intersected directly with commercial alcohol production, at a moment when governments were seeking both revenue recovery and regulatory control after years of prohibition-driven disruption.

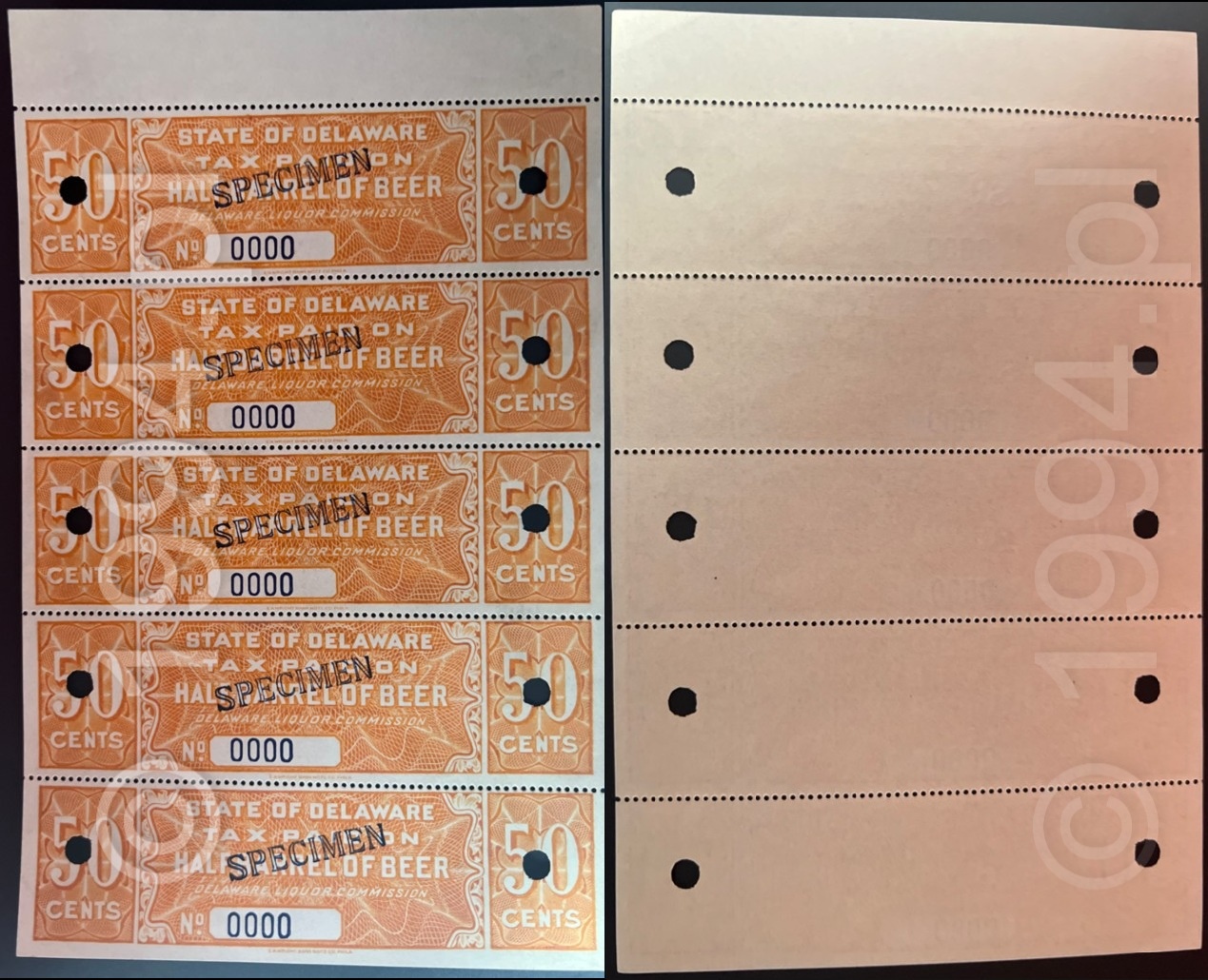

The stamps are printed in orange security engraving and survive here as an intact vertical strip of five impressions on original printer paper. Each individual stamp bears the denomination FIFTY CENTS at both ends and contains a central serial field printed as No. 0000, together with the overprint SPECIMEN. This combination clearly identifies the strip as printer-issued specimen material, produced for approval, reference, or internal control purposes rather than for operational tax payment.

The presence of punch cancellations across each stamp is a critical physical indicator of specimen status. These punches were not part of normal field use but were applied deliberately to invalidate the stamps and prevent their diversion into the taxation stream. Horizontal perforation lines separate the stamps, confirming that the design was intended for individual separation and application during actual use. The reverse is blank, as printed, consistent with adhesive fiscal stamps designed to be affixed to containers or accompanying documentation.

Circulating beer tax stamps from this period were ephemeral by nature. They were separated, applied, soaked off, or destroyed as part of routine commercial practice, leaving little opportunity for survival. Specimen strips, by contrast, existed only briefly within printer or administrative environments during the establishment of the regulatory system and were typically discarded once production was authorized and operational.

The survival of this intact specimen strip therefore carries documentary weight far beyond its nominal function. It captures the precise moment when Delaware’s post-Prohibition alcohol taxation framework was being defined, standardized, and physically implemented. Rather than representing routine tax collection, it documents the reconstruction of state fiscal authority over alcohol in the immediate aftermath of constitutional repeal.

No other specimen strip of this Delaware half-barrel beer tax stamp issue is documented in institutional collections, auction records, or standard fiscal stamp references. Based strictly on observed and recorded evidence, this intact strip stands as a unique surviving example and serves as a primary reference artifact for Delaware’s early post-Prohibition excise taxation system.